- Write by:

-

Tuesday, March 12, 2019 - 2:26:39 PM

-

771 Visit

-

Print

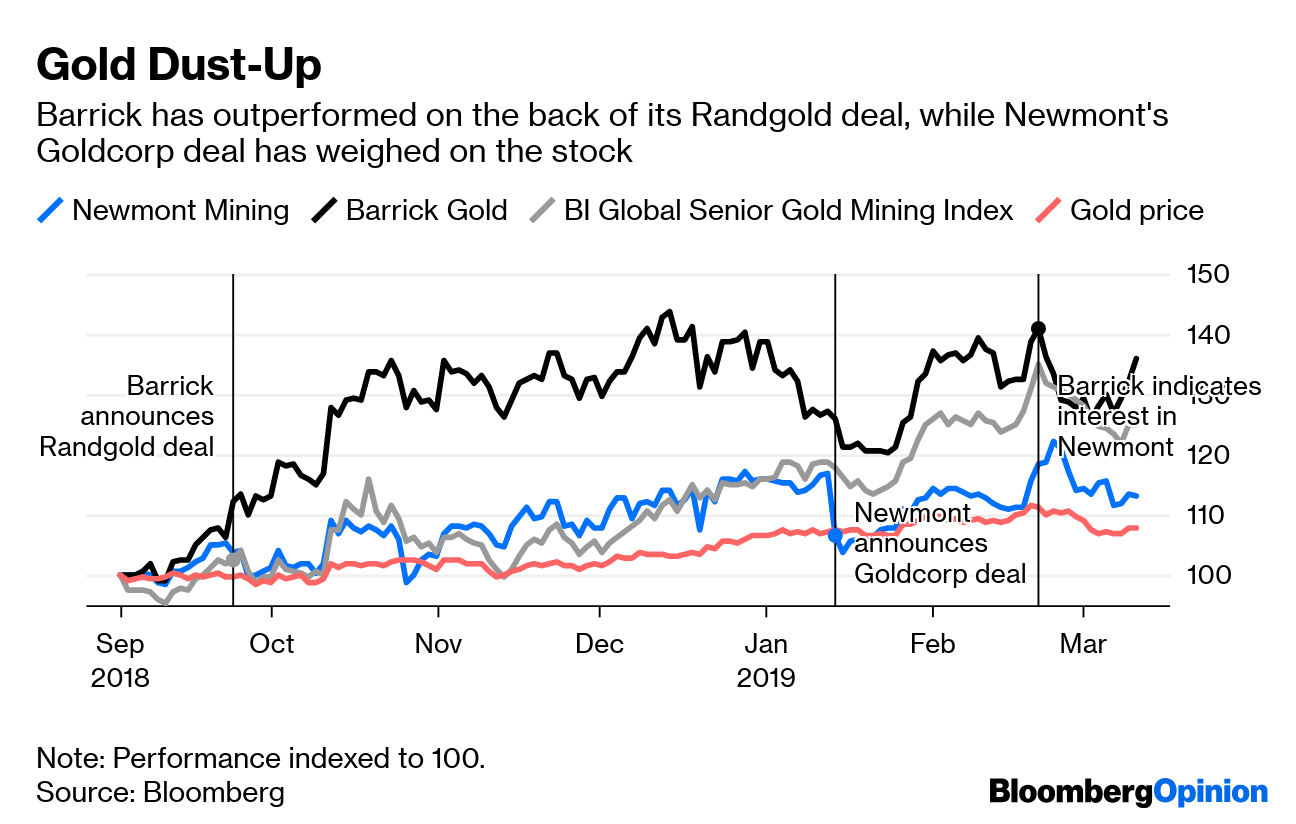

Mining News Pro - It’s amazing what just talking it out can achieve. After a parade of insults, suspect numbers and pitch decks, Barrick Gold Corp. and Newmont Mining Corp. have agreed to a deal. It isn’t the deal Barrick originally pushed for; namely, a hostile full takeover of its rival. Instead, they will holster their Excel models and form a partnership in the one asset anyone really cares about: their Nevada mining operations.

According to Mining News Pro - On balance, it looks as if Barrick got most of what it wanted. It will run the Nevada joint venture and control three of the five board seats governing it. Ownership of 61.5 percent reflects Barrick’s much bigger resource base in the region (as my colleague David Fickling laid out here), with Newmont giving ground on its earlier proposal of a 55/45 split. Meanwhile, Newmont is free to consummate its existing deal to buy Goldcorp Inc. – one that came with a premium that far outstripped original synergy estimates (since revised up, to no one’s surprise.)

Newmont’s shares duly did worse than Barrick’s on Monday morning. But what should concern both companies is just how little regard the market pays to any of this, be it the slagging match or the kumbayas.

Consider: The companies claim the Nevada JV will generate synergies worth $5 billion, discounted over 20 years. I’ve already laid out the, er, optimism underlying their approach when calculating these numbers here. Suffice to say, when it comes to synergies, a 5 percent discount rate and a pre-tax net present value are on the less-conservative end of what is never a very conservative spectrum. Under those assumptions, the synergies would be worth about an extra 11 percent to Barrick’s undisturbed price and 8 percent to Newmont’s. Put on a more conservative 8 percent discount rate and tax the results, and the present value on the synergies gets cut in half and the gain on the disturbed stock prices falls to mid single-digits.

That’s not nothing, of course, especially in a sector where the listlessness of the underlying commodity and competition from exchange-traded funds have put the onus on miners to make their own luck. As the fruit of more than two decades of will-they-won’t-they talks and near misses, though, the impact on value feels incremental rather than transformational. It is still a good outcome, which will be enhanced if the two companies translate the savings into higher dividends as quickly as possible. Yet the episode has also demonstrated just how much blocking and tackling is now required to move the needle on these stocks.

Short Link:

https://www.miningnews.ir/En/News/346173

China’s Zhaojin Mining Industry said on Wednesday that its A$733 million ($477.8 million) offer to buy Australia’s ...

Toronto-listed miner OceanaGold Corp said on Wednesday it will raise 6.08 billion pesos ($106 million) through an ...

Gold’s record-setting rally this year has puzzled market watchers as bullion has roared higher despite headwinds that ...

AbraSilver Resource said on Monday it has received investments from both Kinross Gold and Central Puerto, Argentina’s ...

Gold took a tumble as haven demand waned after geopolitical tensions eased in the Middle East.

The four largest indigenous communities in Chile’s Atacama salt flat suspended dialogue with state-run copper giant ...

A prefeasibility study for Predictive Discovery’s (ASX: PDI) Bankan gold project in Guinea gives it a net present value ...

Representatives from the Peñas Negras Indigenous community, in northwestern Argentina, clashed with heavily armed police ...

Newmont confirmed on Wednesday that two members of its workforce died this week at the Cerro Negro mine located in the ...

No comments have been posted yet ...